Newsletter 30 April, 2026

Amphore Energy Newsletter 30 April 2026

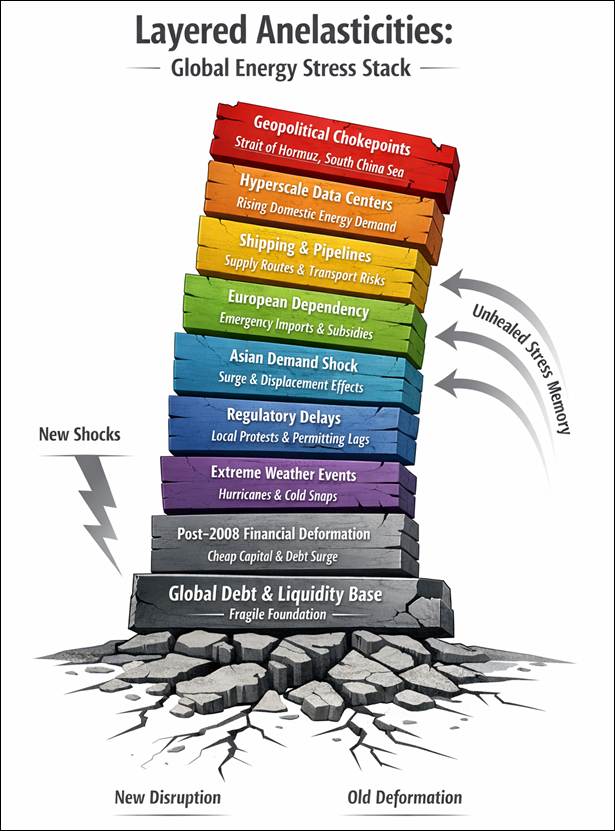

The Gulf has entered a phase where shocks pile up faster than the system can absorb them. Anelasticity is now the rule. Every crisis leaves a scar. Every tension shifts the structure. The system no longer snaps back. Hysteresis sets in. The past dictates the present.

The UAE’s exit from OPEC and OPEC+ belongs to this logic. It is not tactical. It is structural. It marks the end of the old balance. The long fight with Saudi Arabia over quotas is no longer a technical quarrel. It is a clash of strategies. It is a collapse of trust. That collapse has spread from Yemen to the Horn of Africa to North Africa. It now reaches the core of Gulf oil governance.

Saudi Arabia wants to hold the marginal barrel. The UAE wants production freedom and a central role in the next energy system. The break comes at record oil prices. That alone shows the depth of dysfunction. Even extreme prices cannot mask accumulated fatigue. Markets still carry the memory of past shocks. They move with delay, inertia, and volatility. Classic hysteresis.

Around this fracture a new industrial race is taking shape. The Gulf is no longer competing only on oil. It is competing on molecules. Hydrogen becomes a long‑term hedge. Ammonia becomes the export vector for Asia. CO₂ management becomes a strategic capability. Saudi Arabia pushes blue hydrogen and ammonia tied to NEOM and CCS hubs. The UAE builds certification chains and port‑based ammonia corridors. Qatar links LNG expansion to blue hydrogen and CO₂ reinjection. Oman bets on green hydrogen anchored in low‑cost solar. Each state locks in a different technological path. Each path defines a different geopolitical future.

Iran enters the race as well. It uses hydrocarbons, minerals and geography to reinsert itself into regional flows. It treats hydrogen and ammonia as tools to bypass sanctions and reconnect with Asia. The Gulf monarchies and Iran are no longer exporters. They are becoming designers of molecules, processes and logistics.

This shift now intersects with the United States. Washington extends its energy reach from the Eastern Mediterranean to the Indian Ocean. It uses flexible LNG massive hydrogen incentives and control over future export corridors to Asia. The Gulf monarchies and Iran move in parallel. They want their own corridors, markets and industrial chains. The competition is now open. It is about who supplies Asia’s next energy cycle and who controls the CO₂‑managed value chains that underpin it including hard‑carbon production pathways and the new electricity‑storage systems built around captured and recycled carbon.

In this landscape the UAE’s departure from OPEC+ becomes a geopolitical marker. The unified Gulf oil policy is over. A decade of accumulated anelasticity has crossed into hysteresis. This new condition will shape post‑conflict strategies, alliances, prices and flows. Energy again becomes the central lens through which global power must be read.

https://www.naftemporiki.gr/opinion/2104194/apo-to-vareli-sta-kainoyrgia-proionta-o-viomichanikos-polemos-toy-kolpoy-gia-ton-epomeno-energeiako-kyklo-tis-asias/