Rigid Margins, Rising Pressures: The New Gulf Gas Order

The global gas system is entering a phase defined by limits rather than freedoms. It absorbs shocks but does not return to a neutral baseline; each disturbance leaves a mark that becomes part of the next equilibrium. The United States and Qatar may appear flexible from afar, yet their room for maneuver is narrow. They can redirect LNG only within the boundaries set by sunk investments, long‑term contracts, and political alignments. Once capacity is built, it cannot unwind. The system moves slowly, adjusts reluctantly, and carries the memory of every shift.

The Hardening Global Gas System

The system’s rigidity is now more visible. The United States is expanding LNG capacity to rival Qatar by 2030, yet the pace is slowed by the geography of its own production chain: gas must move from inland basins to coastal liquefaction plants through a network that was never built for sustained export surges. Pipeline congestion, slow permitting, and local resistance limit how quickly feed gas can reach the coast, while AI hyperscale data centers and electrification pull more gas into the domestic grid. The result is a tightening export margin even as nominal capacity rises. Qatar faces its own friction. Damage to upstream and processing facilities has introduced delays, and repairs move at the pace of overstretched contractors and slow supply chains. Even the most efficient exporter cannot escape the mechanical realities of maintenance. The sense of fluidity fades; the global gas system behaves less like a market adjusting around price signals and more like a structure settling into a heavier, more permanent form.

Constraints That Redraw the Map

The emerging gas landscape is defined as much by its boundaries as by its volumes. The Gulf’s constraints stem from geography, domestic consumption, and political architecture. These pressures do not weaken the system; they shape it. For the Gulf, the central constraint is internal absorption. Iran and Saudi Arabia cannot release gas for export without altering their social contracts. The UAE’s outward ambitions require a tighter domestic balance. Oman’s industrial strategy locks in new loads. Kuwait remains structurally short. These are not passing stresses but enduring features that turn every decision into a one‑directional move. Qatar faces its own structural limits. Infrastructure damage slows expansion, repairs take time, and supply chains drag. Even Qatar cannot escape the inertia of its own system. Together, these pressures create a new geometry: the Gulf cannot expand freely, and both regional and external suppliers settle into firmer, more permanent shapes. The global gas map becomes a map of boundaries rather than options.

The Gulf’s Irreversible Geometry

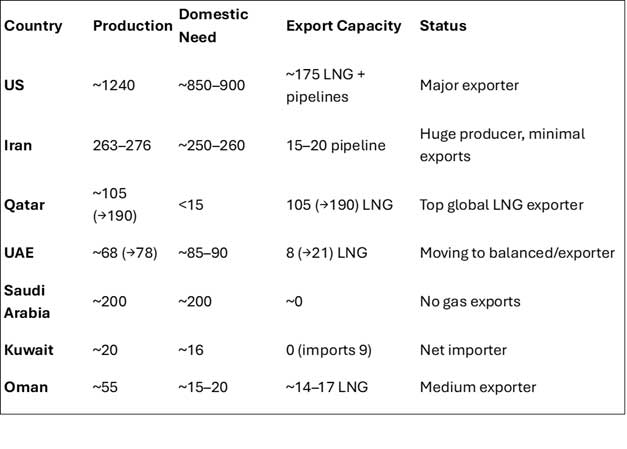

Iran and Saudi Arabia form the dense core of the region’s gas world. They produce huge volumes and consume almost everything domestically. Their economies run on cheap gas, and freeing molecules for export is not a technical adjustment but a political reallocation of scarcity. It cannot be reversed. If Iran ever exports significant gas or hydrogen, it will follow rationing and reform choices that will reshape the state permanently. Saudi Arabia faces the same logic with Jafurah: once gas feeds blue hydrogen, petrochemicals, or power, the pattern hardens. The table highlights how each producer carries its own structural balance between output, domestic absorption, and export reach.

Qatar is at the other end. It looks outward more than any Gulf supplier, but its freedom to move is still limited. North Field expansions are multi‑decade commitments. Once trains and ships are built, they cannot be undone. Qatar cannot cut exports without harming its fiscal base, nor can it redirect volumes without rewriting its Asian portfolio. Flexibility exists only at the margins. The core is fixed. This rigidity now meets U.S. rigidity: two export giants, two irreversible trajectories, both targeting Asia, both facing delays, both constrained by internal pressures. Competition becomes deformation rather than adjustment.

Qatar is at the other end. It looks outward more than any Gulf supplier, but its freedom to move is still limited. North Field expansions are multi‑decade commitments. Once trains and ships are built, they cannot be undone. Qatar cannot cut exports without harming its fiscal base, nor can it redirect volumes without rewriting its Asian portfolio. Flexibility exists only at the margins. The core is fixed. This rigidity now meets U.S. rigidity: two export giants, two irreversible trajectories, both targeting Asia, both facing delays, both constrained by internal pressures. Competition becomes deformation rather than adjustment.

The UAE and Oman occupy transitional positions. The UAE is shifting from importer to hub, a one‑way transformation shaped by Dolphin gas, Ruwais LNG, and rising domestic demand. Once the UAE becomes a hub, it cannot return to its earlier configuration. Oman reflects the same dynamic: contractual commitments and industrial clusters create momentum, so disruptions shift the system’s path instead of sending it back. Kuwait represents the clearest case of structural shortfall. It relies on LNG imports, and every shock, weather, price spike, or shipping disruption leads to rationing and fuel switching. New fixes become permanent. The system never relaxes.

Across the region, the Gulf behaves like a material that settles into new forms under pressure. Oil cycles, sanctions, LNG tightness, climate policy, and Hormuz tensions carve channels and create new baselines. Iran’s exclusion from exports created a domestic demand engine that now shapes its entire posture. Qatar’s rise created a fixed anchor. Saudi Arabia’s internalization of gas locked in roles. These roles will not reverse. Global forces reinforce them: United States–Qatar dual rigidity, AI-driven U.S. demand, pipeline delays, and Qatar’s infrastructure repairs all contribute to a system that carries the memory of every shock. Finally, and reinforced by last‑minute developments, Iran has tightened its strategy and begun opening small, gradual corridors of easing with its neighbors, a shift shaped not only by Kuwait’s structural vulnerability but also by China’s preference for a calmer Gulf that protects its long‑term energy corridors.

In such a world, cooperation is not about restoring balance but managing irreversible shifts. Gulf coordination will not recreate flexibility; it will codify the scars already present. Hormuz arrangements will formalize Iran’s role. Hydrogen and ammonia standards will anchor Qatar and the UAE as certifiers. Pipeline swaps will embed Iran and Oman into specific corridors. Each agreement reduces volatility but deepens the system’s memory. The underlying logic is clear. The global gas world is not a flexible market but a structure shaped by inertia, memory, and irreversible choices. Every investment leaves an imprint. Every crisis leaves a trace. Every pipeline and LNG train becomes part of the region’s geometry. Qatar remains the anchor exporter. Iran stays the constrained giant, and the war has only reinforced this, turning its structural limitations into a decisive factor in the Gulf’s long‑term equilibrium. Saudi Arabia absorbs its own gas to protect its oil. The UAE grows into a regional hub. Oman holds its steady mid-tier role. Kuwait remains structurally short. The United States stands as the external pole, tightened by AI‑driven domestic demand and slowed by infrastructure delays. Any cooperative architecture must begin from this reality. The system will not snap back. It will move forward, carrying the memory of every shock and the weight of every decision.

Read the entire article in Greek or translate below

Modern Diplomacy / Oil & G, Friday, May 8, 2026

Rigid Margins, Rising Pressures: The New Gulf Gas Order - Modern Diplomacy

Watch the video below