The New Order of Natural Gas in the Gulf: Established Roles, Limited Room for Maneuver

The U.S. and Qatar appear to be flexible players, but in practice they operate within narrow constraints imposed by infrastructure, long-term contracts, and political commitments. Their flexibility is mainly an illusion, not reality, as any change in flows takes time and leaves a lasting mark on the system’s operation.

The Changing Gas Market in the Gulf

The system’s inflexibility is now becoming apparent. The U.S. is expanding LNG capacity to compete with Qatar by 2030, but supply to coastal terminals is constrained by pipeline geography, permitting, and rising domestic demand. Hyperscale data centers and electrification are absorbing an ever-larger share, reducing the gas available for exports, with the result that the actual export margin is narrowing even as nominal capacity increases.

Qatar is facing different kinds of challenges. Damage to refining, liquefaction, and processing facilities is causing delays, while repairs are proceeding at the slow pace of contractors and supply chains. Even the most efficient exporter cannot escape the time-consuming burden of maintenance, with the result that the system resembles less an adaptive market and more a cumbersome structure.

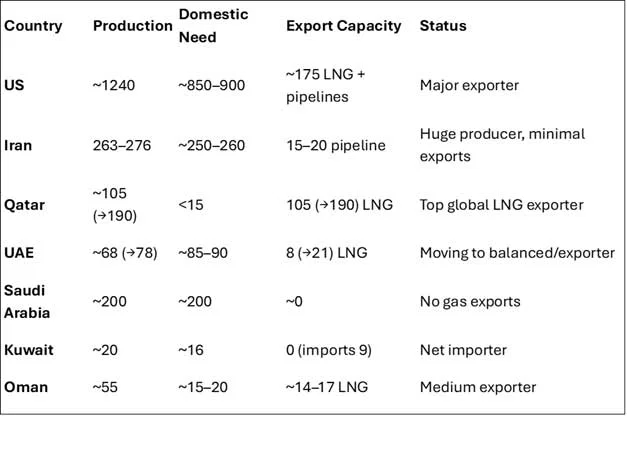

The Gulf’s constraints stem from geography, domestic consumption, and political architecture. Iran and Saudi Arabia cannot release gas for export without altering their social contract, while the UAE’s outward-looking plans require a stricter internal balance. Oman’s industrial policy consistently allocates new volumes to the domestic market and exports, while Kuwait continues to face a persistent gas deficit. The result is a new dynamic in which the Gulf operates within defined boundaries and suppliers are entrenched in roles that are difficult to change.

The Consolidation of Boundaries in the Gulf

The Consolidation of Boundaries in the Gulf

Iran and Saudi Arabia are the cornerstones of the Gulf’s natural gas sector because they produce large volumes, yet consume almost all of it domestically. For both countries, making gas available for export is not a technical issue but a political choice concerning the balance between domestic demand and exports. In Iran, substantial exports of natural gas or hydrogen would require deep domestic reforms, while Saudi Arabia is reserving gas for blue hydrogen, petrochemicals, and power generation, thereby cementing its current structure.

At the same time, the global natural gas system is becoming more rigid, as disruptions are not absorbed but incorporated, creating new points of equilibrium with limited flexibility. The U.S. and Qatar are operating within tight constraints, with U.S. flows constrained by pipeline geography and rising domestic demand, while Qatar moves at the pace dictated by its technical infrastructure and portfolio commitments. In the Gulf, the balance is determined by domestic consumption and political priorities; Iran and Saudi Arabia absorb nearly all of their production, the UAE needs a steady supply for its role as a hub, Oman reserves shipments for its industrial strategy, and Kuwait remains permanently in deficit. The result is a system where even the largest exporters operate within limits and regional roles are cemented.

The New Geometry of the Gulf

The roles in the Gulf have now stabilized. Iran remains a major producer with minimal exports due to domestic demand created by its isolation; Saudi Arabia reserves all its gas from the Jafurah facilities for domestic use; Qatar maintains its position as a central hub for LNG, the UAE is evolving into a regional hub, Oman remains a stable mid-tier player, and Kuwait continues to be vulnerable to fluctuations. The U.S. functions as an external pole, but its own inflexibility, domestic demand, and infrastructure delays converge with Qatari delays, creating a bipolar stability with limited adaptability, as both target Asia.

Pressures arising from oil cycles, sanctions, LNG shortages, climate policies, and tensions in the Straits are leaving a lasting mark. Qatar’s rise acts as an anchor; Saudi Arabia’s domestic gas production is stabilizing roles, while Iran’s potential gradual rapprochement with neighbors reflects the need for regional calm that benefits China and eases pressure on Kuwait.

In this environment, cooperation does not restore old balances but manages ongoing realignments. Arrangements in the Strait can institutionalize Iran’s role, while standards for hydrogen and ammonia strengthen Qatar and the UAE as countries that set the rules for the new trade. At the same time, volume-sharing agreements between Iran and Oman could integrate both countries into specific energy corridors. Any such arrangement reduces short-term volatility, but at the same time adds new commitments that make the system more rigid and less capable of changing course in the future.

Read the entire article in Greek or translate below.

NAFTEMPORIKI / OPINIONS, Sunday, May 9, 2026

Η Νέα Τάξη του φυσικού αερίου στον Κόλπο: Παγιωμένοι ρόλοι, περιορισμένα περιθώρια